I want to start with a number that I think about a lot. CB Insights tracks the post-mortems of companies that shut down. In their most recent analysis, looking at 431 venture-backed startups that went under since 2023, 70% of founders cited running out of capital as the cause of death.

70%. Not 30%. Not half. Almost three out of every four.

Now, the obvious objection is that running out of cash is usually the symptom, not the disease. The disease was that the product had no market, or the team was wrong, or the timing was bad. That is true. But it is also true that a lot of these businesses ran out of cash sooner than they had to. They ran out of cash before they got the chance to fix the underlying problem. And the reason they ran out sooner than they had to is, almost always, that nobody in the room had a clear, current picture of how much cash they had and when it was about to disappear.

I want to be clear about what a 90 day cash flow forecast is and is not. It is not a fundraising tool. It is not a strategic plan. It is not a five year model. It is the most boring, operational document you will own. It is also the one document that, if you maintain it honestly, will keep you out of the 70%.

What a 90 day cash flow forecast actually is

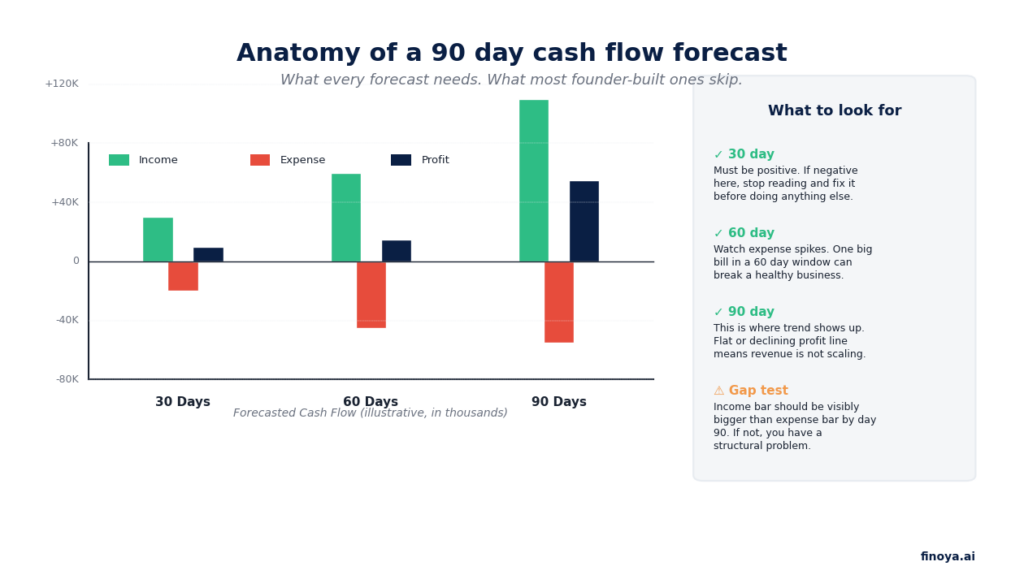

A 90 day cash flow forecast is a week-by-week or month-by-month projection of every dollar coming in and every dollar going out of your business over the next 13 weeks. The goal is not to predict the future perfectly. The goal is to know, at any given moment, the answer to one question: “If nothing changes, when do I run out of cash?”

If you can answer that question in five seconds, you have a working forecast. If you cannot, you do not.

The reason 90 days is the right horizon, not 30 and not 6 months, is that 90 days is long enough to see a problem coming and short enough that the numbers you are projecting still mean something. A 30 day forecast is a bank statement. A six month forecast is wishful thinking dressed up as a spreadsheet. 90 days is the operating planning horizon.

Every 90 day forecast worth using has four components. First, opening cash position. The number in your bank account today, across all accounts. Second, projected money in. Customer payments due, based on actual outstanding invoices and historical collection rates. Third, projected money out. Payroll, rent, software subscriptions, supplier bills, tax payments, and the other non-negotiable monthly costs. Fourth, the running cash balance. Opening cash, plus projected in, minus projected out, week by week.

If your running cash balance ever turns negative inside the 90 day window, that is a flag. You have somewhere between zero and 12 weeks to fix it. The further out the negative number is, the more options you have. The closer it is, the fewer options. This is why looking at the forecast weekly matters more than looking at it monthly. A weekly look gives you 12 chances to course correct. A monthly look gives you 3.

The two methods, and why most founders pick the wrong one

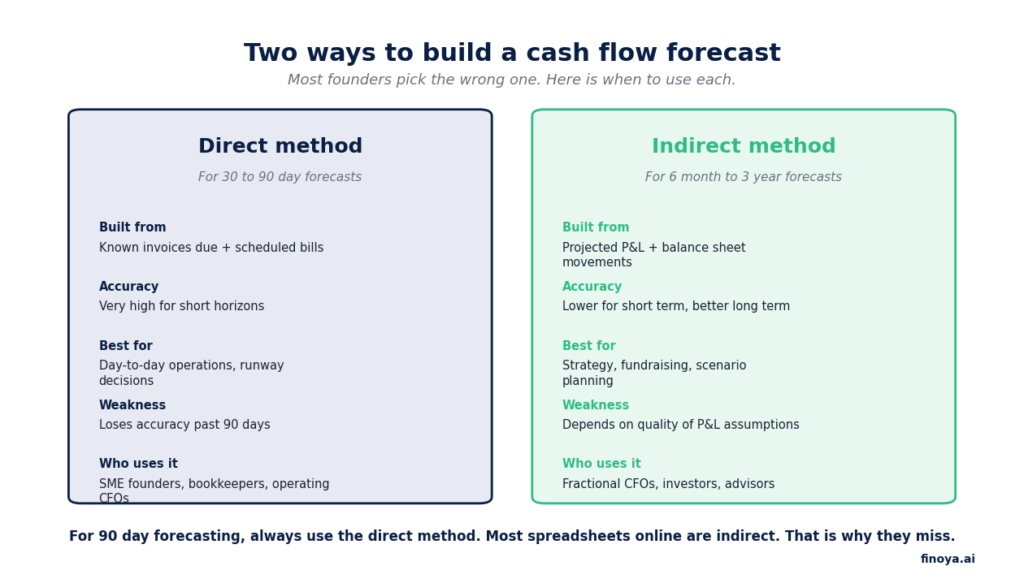

There are two ways to build a cash flow forecast. The direct method and the indirect method. They sound similar but they answer fundamentally different questions, and using the wrong method is one of the most common reasons founder-built forecasts fall apart inside the first month.

The direct method builds the forecast from actual scheduled cash events. Customer A owes you $42,000 due on the 15th. Payroll runs $87,000 on the 30th. Rent is $14,000 on the 1st. Each line item is a real, dated cash event tied to either an invoice or a recurring obligation. You add them up by week. The output is what is going to actually happen with your bank balance, give or take collection timing.

The indirect method builds the forecast from your P&L and balance sheet. You take projected revenue, subtract projected expenses, adjust for changes in working capital, and arrive at projected cash flow. It is mathematically valid but it depends entirely on the accuracy of your P&L assumptions, which for short horizons are usually wrong.

Most spreadsheets you can download online are built on the indirect method, because that is the method finance textbooks teach. For 90 day forecasting, the indirect method is the wrong tool. Use the direct method. Build from invoices and bills. Your forecast will be 10 times more accurate and 100 times more useful.

Why most founder-built forecasts fail in the first month

I have seen probably 50 different small business cash flow spreadsheets in the last two years. Almost all of them have the same three problems.

First, they are static. The founder builds the forecast in January, looks at it once or twice in February, and by March it is so out of date that it is actively misleading. A forecast that is not updated weekly is not a forecast. It is a historical document with delusions of grandeur.

Second, they assume customers pay on time. They do not. The average small business in the US gets paid 23 days late on net 30 invoices, and longer on larger ones. If your forecast assumes invoices land on the day they are due, your forecast is consistently overoptimistic by about three weeks of cash.

Third, they ignore the lumpy stuff. Quarterly tax payments. Annual software renewals. The big insurance premium that hits in November. A forecast that only models the smooth monthly line items will look healthy right up until a $40,000 bill nobody planned for arrives in the second month.

The five scenarios you need to run, every quarter

A forecast is a base case. The base case is what happens if everything goes more or less as planned. The whole point of having a forecast is that you can stress test it against the things that might actually go wrong, or the moves you are considering making, before you commit.

These five scenarios are not exhaustive. They are the minimum you should be able to run. The reason they matter is that the answers expose the structural fragility of your business in a way that the base case never does. A business that looks healthy in the base case but cannot survive a single big customer churning is fragile. A business that needs three of these scenarios to be wrong before it gets in trouble is robust. The forecast tells you which kind you have.

Most founders I talk to cannot run any of these scenarios in less than a day, because their forecast is in a spreadsheet that breaks if you change one input. That is the core problem. A forecast that takes a day to flex is a forecast you will not flex.

How we built this into Finoya

When we built the cash flow forecasting feature in Finoya, we made three deliberate decisions about how it would work. Each was a reaction to one of the failure modes above.

We made it dynamic. The forecast updates automatically every week. There is no “refresh the spreadsheet” step.

We made the collections honest. We use your actual historical payment patterns by customer to predict when invoices will land. If Customer A pays you on average 18 days late, our forecast assumes 18 days late, not the contractual 30. This means your forecast deflates the optimistic line everyone else’s forecasts have.

We made the scenario testing instant. The five scenarios above run as buttons. You click “big customer churns,” pick the customer, and the forecast redraws in real time. You can run all five in two minutes. If you can run them in two minutes, you actually run them. That is the entire point.

What you should do this week, regardless of whether you use Finoya

If you have a forecast, open it. Check whether it is accurate as of today. If it has not been updated in two weeks, update it. If updating it takes more than 30 minutes, your forecast is not built right and you should rebuild it on the direct method.

If you do not have a forecast, build one. Even a rough one in a spreadsheet is better than nothing. Open a sheet, write your opening cash balance at the top, list every customer invoice that is outstanding with its expected pay date, list every recurring bill for the next 13 weeks, and watch the running balance line move. The first time you do this is uncomfortable. Most founders learn that they are more exposed than they thought. That discomfort is the value.

If you want to skip building it from scratch, you can connect Xero or QuickBooks to Finoya and have a working 90 day forecast in under 10 minutes. Seven days free, no credit card. Start at app.finoya.ai.

If your books are not in good enough shape to forecast against (you would be surprised how many small businesses are in this category), you can find a vetted bookkeeper or accountant in our marketplace. Free to browse. marketplace.finoya.ai.

The forecast is not a one-time exercise. It is a weekly habit. The founders who build the habit are not the smartest founders, or the best capitalised, or the luckiest. They are the ones who decided that 70% was not going to be them.